Stop maxing your 401k. Seriously. Do this first.

Your financial advisor won’t tell you this because it literally reduces their paycheck. But the IRS already wrote the playbook — most people just skip steps 1-3.

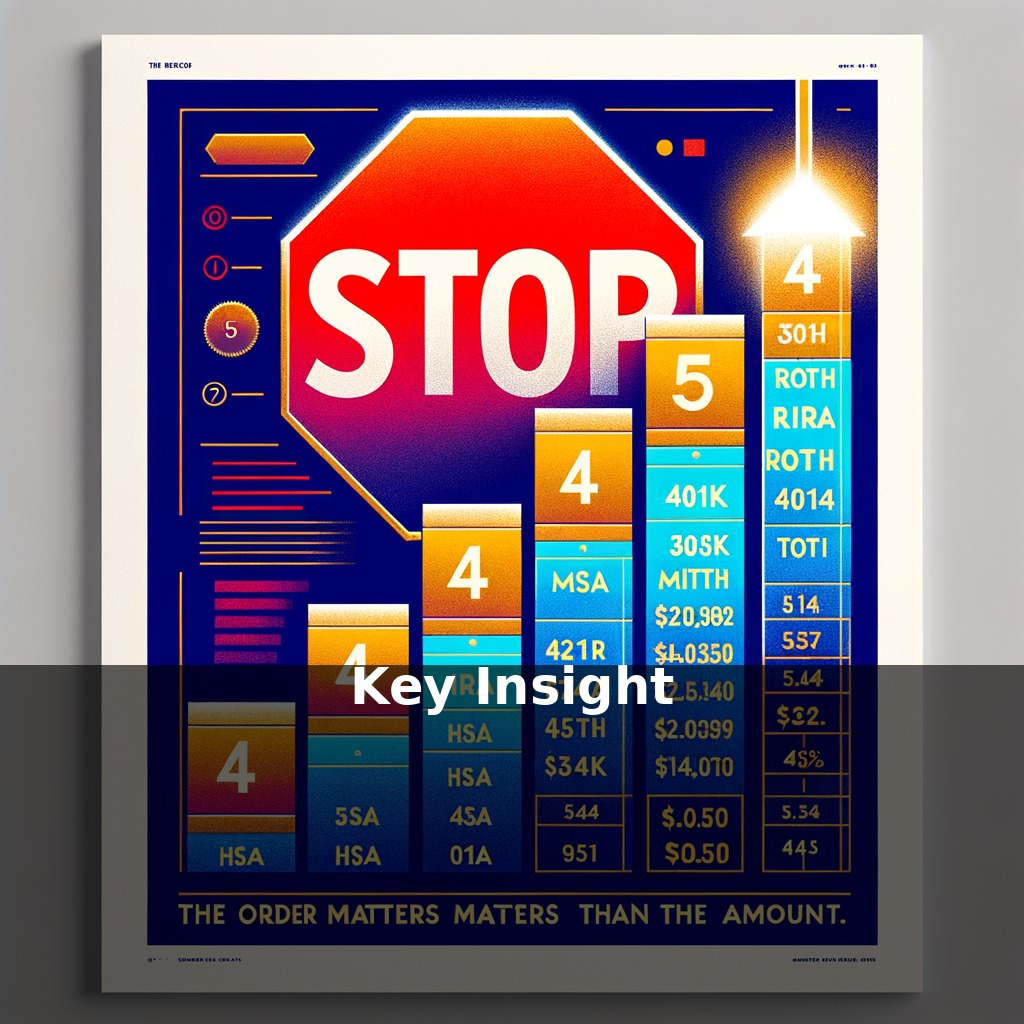

Here’s the REAL wealth priority ladder 👇

1️⃣ HSA FIRST (if eligible)

Triple tax-advantaged. Tax-free in, tax-free growth, tax-free out for medical. It’s the only account in America that does that. Max this before anything else.

2️⃣ 401k MATCH (only up to the match)

If your employer matches 4%, contribute 4%. Not a penny more yet. That match is a 100% instant return — you’d be insane to leave it.

3️⃣ ROTH IRA

Pay taxes now at today’s rates (historically low) so your money grows tax-free forever. $7k/year limit in 2024. You control the investments — not your employer’s overpriced fund menu.

4️⃣ THEN max your 401k

Now you can stuff the rest into your 401k for the tax deduction. But notice — it’s step 4, not step 1.

5️⃣ Bonus: Roll old 401ks into an IRA

Got a 401k sitting at an old job bleeding fees? Tools like Capitalize make rollovers free and take 10 minutes.

Why doesn’t your advisor mention HSAs or Roth IRAs? Simple — they don’t manage those accounts, so they don’t earn AUM fees on them. Follow the money.

The order matters more than the amount. Someone investing $300/month in the RIGHT order will out-earn someone investing $800/month in the wrong order over 30 years.

💬 Which step are you stuck on? Drop a number in the comments and I’ll help you map it out.

📌 Save this so you don’t forget the order.

Follow @WealthFlowDaily for the money playbook they didn’t teach you in school.

💰 Refer someone to OfferLab and earn up to 2% lifetime & $497 upfront commissions — Refer someone to OfferLab and earn up to 2% lifetime & $497 upfront commissions

👆 Link in bio to get started!

Save this so you don’t forget the order — and comment the step you’re stuck on.

Send free SMS worldwide

Reach any mobile number in 200+ countries from your browser. No signup, no app.

Send a free SMS →